The birth of the ACH network

In the 1970s, the Federal Reserve and banking industry began to look for solutions to improve the paper check system. Compared to the speed of wire transfers, paper checks took a long time to process. Plus, their volume was increasing, which was straining the system.

Fed Governor George Mitchell (Off-site) suggested that electronic technology could provide more efficient functional performance. Clearing houses were already facilitating the exchange and settlement of payments, but with the addition of an electronic mechanism (Off-site), the automated clearing house was born as a solution (Off-site).

The first ACH began operating in the Federal Reserve Bank of San Francisco in 1972 and the FedACH Service came to life. The number of automated clearing houses operated by the Federal Reserve grew across the United States and by the 1990s, the Fed consolidated them into one national network (Off-site).

Increasing the speed of the FedACH Service

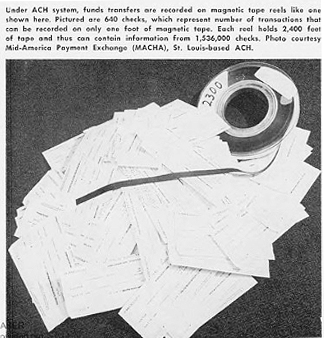

At first, FedACH Service transactions were transmitted through physical media, such as magnetic tapes and floppy disks. A single magnetic tape could contain the equivalent of 1.5 million checks, yet the process could still be cumbersome. Therefore, routine payments like payroll or bills were the most common transaction type.

Eventually, the use of physical media became a barrier to speed and in 1993, the Federal Reserve Board required all FedACH Service participants to establish an electronic connection (Off-site). This change led to an increase from processing one batch of transactions per day to six a day by 2023.

The current state of ACH

Today, the FedACH Service is an integral part of the payment system, allowing for electronic bank-to-bank transfer of funds. In 2024, the service facilitated the transfer of more than $42 trillion (Off-site), with payroll, bill pay, internet-based and business-to-business payments as the most common transaction types. In addition, the FedACH Service has grown to include a robust suite of products, including transaction, information and fraud mitigation services.

To learn more about the history of the FedACH Service, visit Federal Reserve History: Automated Clearing House Payments (Off-site).