2025 Diary of Consumer Payment Choice

In May, Federal Reserve Financial Services’ FedCash® Services released the annual Diary of Consumer Payment Choice (PDF) report from its ongoing research into the payment habits of U.S. consumers. The 2025 findings from this nationally representative survey showed that amid increasing digitalization of payments, consumers continue to use cash and keep it handy.

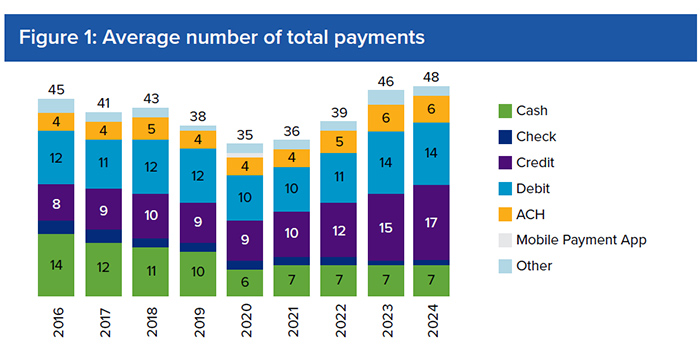

Overall, U.S. consumers made an average of 48 payments per month in 2024, continuing an upward trend that began in 2021. Increased credit card usage, remote payments and payments made with mobile devices fueled growth in the overall number of payments.

Within this evolving payment landscape, cash use remained stable. In 2024, consumers made an average of seven payments per month with cash, a number that has remained unchanged since 2020. Additionally, cash was the third-most-used payment instrument after credit and debit cards, a position it has held for the past five years.

The study also revealed generational and demographic trends in payments. Households earning less than $25,000 per year and adults 55 and older relied more on cash than other cohorts. In contrast, adults aged 18 to 24 were more likely to pay with a mobile phone, using their phones for 45% of all payments.

Other key findings included:

- In 2024, cash accounted for 14% of all consumer payments by number, while credit and debit cards accounted for 35% and 30% of payments, respectively.

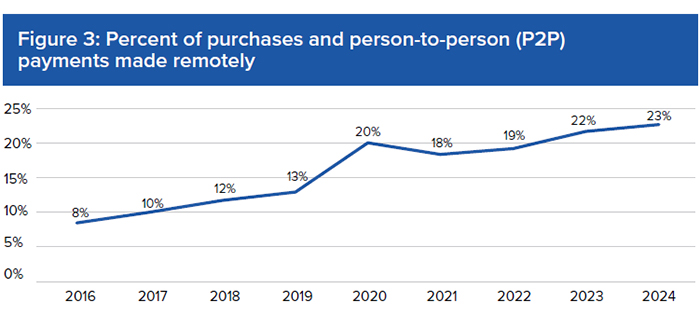

- 23% of consumer purchases and peer-to-peer payments were made remotely in 2024, a share that has increased each year since 2021.

- U.S. consumers made an average of 11 payments per month with a mobile phone in 2024, up from four payments since 2018.

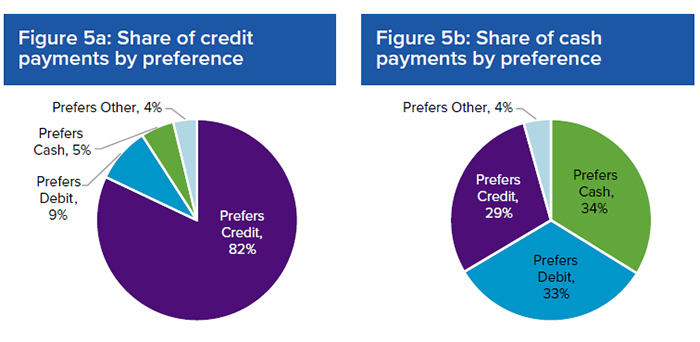

- Cash remains a key backup payment method for U.S. consumers. Of all cash payments in 2024, nearly two-thirds were made by consumers who prefer other payment methods such as debit or credit cards.

- Nearly 80% of U.S. consumers have held cash in their pockets, purses or wallets for at least one day of the month for each Diary survey conducted since 2018. Though the value of these holdings has decreased since 2022, it remained elevated in 2024 compared to pre-pandemic levels.

- More than 90% of U.S. consumers intend to use cash as either a means of payment or store of value in the future.

Since 2016, the Federal Reserve has conducted this annual consumer survey each October to better understand the payment habits of U.S. consumers. Participants report all payments over a three-day period, the value of their cash holdings, payment instruments used and their preferences for various types of payments.

About the Diary of Consumer Payment Choice

The Federal Reserve conducts the Diary of Consumer Payment Choice survey every year to understand U.S. consumers’ payment behavior, preferences and how consumer payments change from one year to the next. The latest survey was conducted in October 2024. Understanding the evolving role of cash in the U.S. economy through the Diary studies helps ensure FedCash Services is fulfilling its mission of meeting cash demand in times of both normalcy and stress, maintaining the public’s confidence in U.S. currency, and providing ready access to cash.

Federal Reserve Financial Services uses data from the Diary to understand consumer cash use and anticipate its ongoing role in the payments landscape. By tracking consumer payment transactions and preferences annually during the month of October, Federal Reserve Financial Services compares cash with other payment instruments, such as credit and debit cards, checks and electronic payment options. Diary participants also report the amount of cash on hand after each survey day, cash stored elsewhere and cash deposits or withdrawals. Analysis of the Diary data includes the impact of age and income on an individual’s payment behavior and preferences, as well as cash stocks and flows at an individual level.